When are Home Prices Going to Come Down?

When Are Home Prices Going to Come Down?

I get this question on just about every tour. We'll be driving through Cave Creek or pulling up to a place in the West Valley, and somewhere between the second and third house it comes out: "Patty — be honest. When are prices finally going to drop?"

And I love that question, because it means you're thinking like a buyer who wants to do this right. So let me put on my tour-guide hat and walk you through how I actually see it — no scare tactics, no crystal ball, just me laying the map out on the table.

Everybody remembers the last time home values ran up like this. They shot up, and then they fell right off a cliff. So it makes total sense that people are bracing for a repeat. But here's the thing I keep coming back to: I don't think this run is built the same way that one was. Let me show you why.

First, the part that still blows my mind

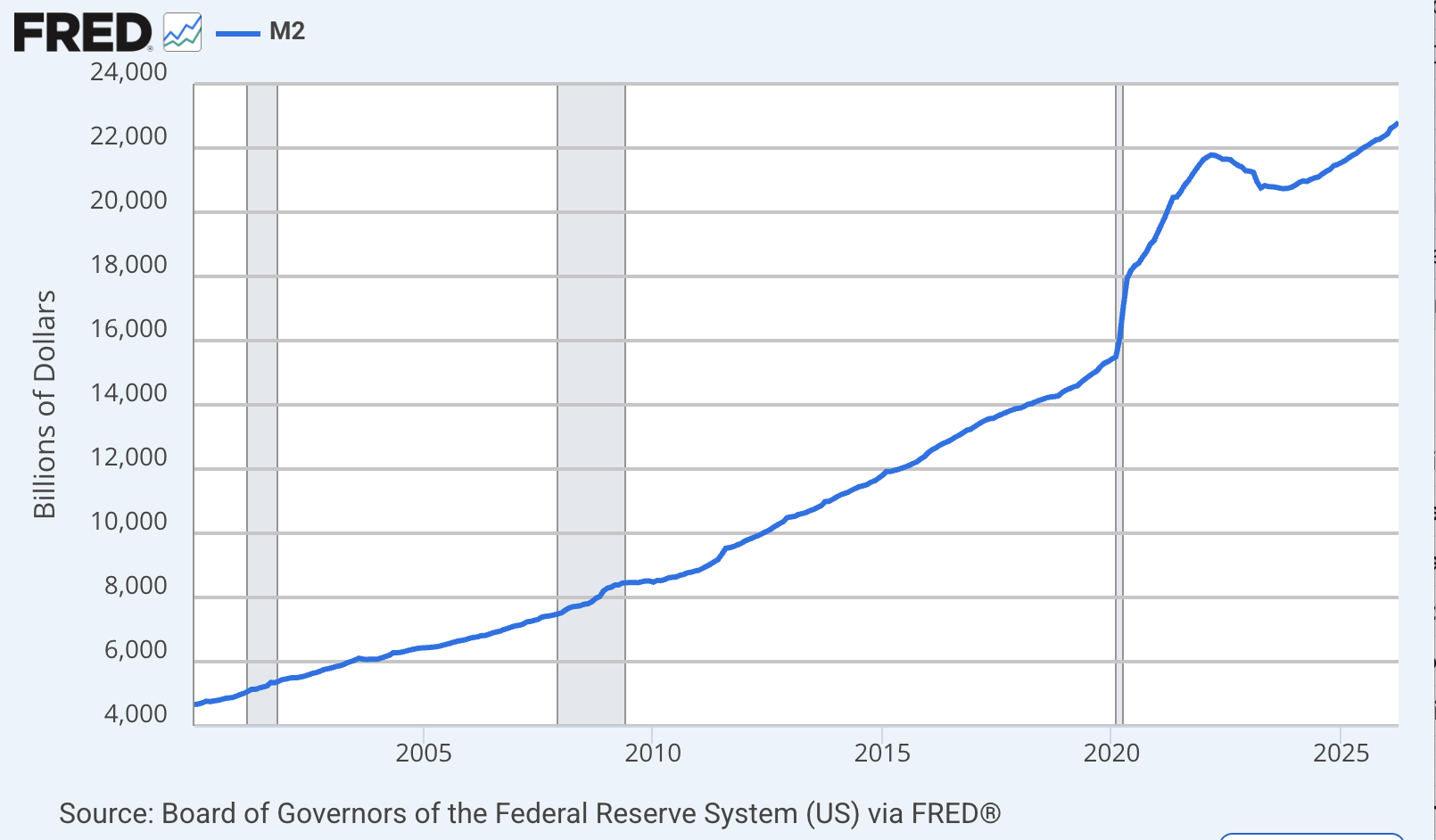

When the world shut down, the government put an enormous amount of money into the economy — somewhere in the neighborhood of $6,000,000,000,000. Six trillion dollars. Look at all those zeros.

And that, more than anything, is the oddity behind this last spike in home values.

So why is this cycle different?

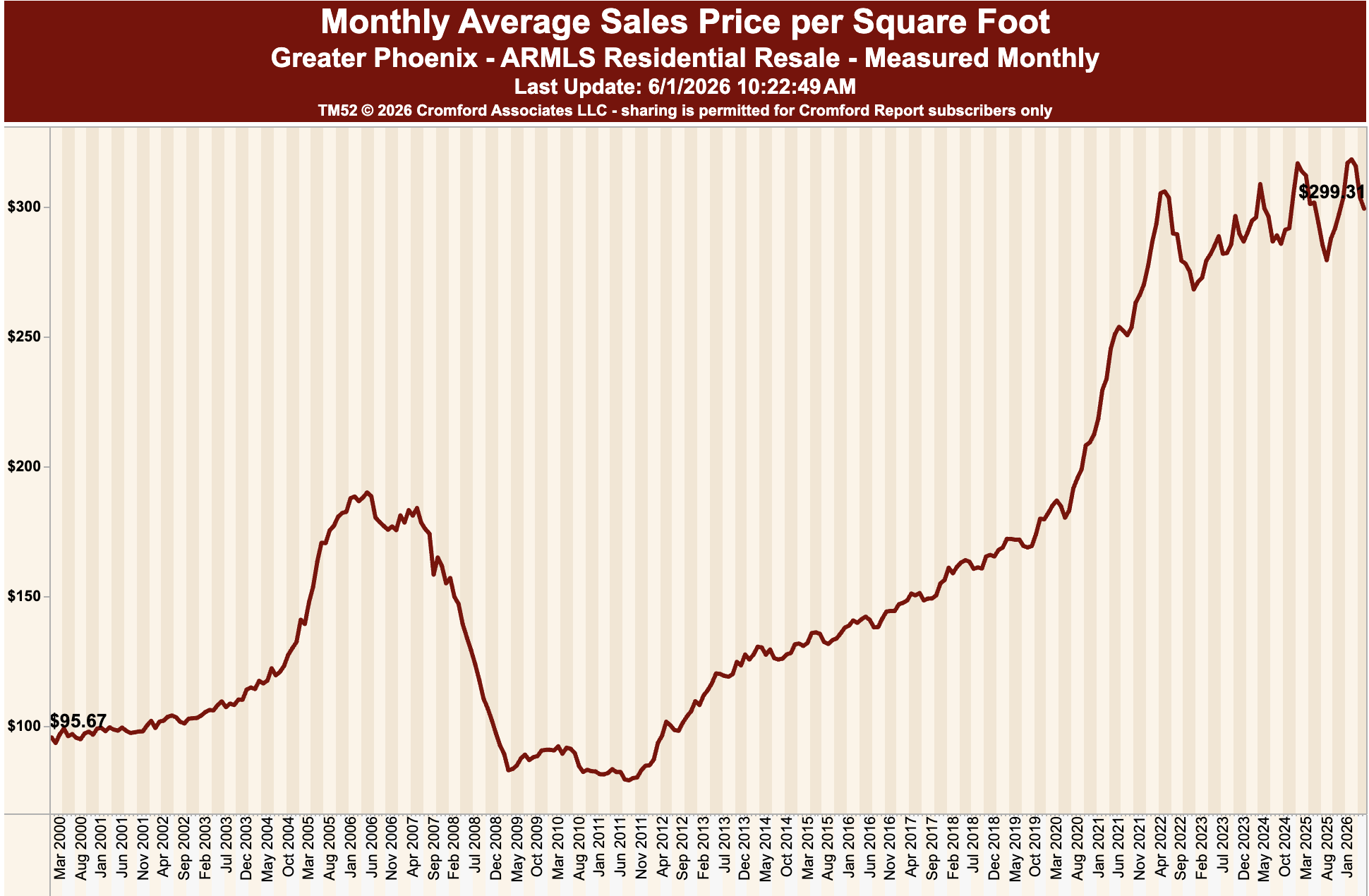

If you've ever fallen down the FRED chart rabbit hole, you know the data folks practically live there. I'll peek at their real estate charts now and then — they're usually a little out of date and too broad to be all that useful for a specific neighborhood, but they're great for the big-picture history. Today I want to look at a different one. The money chart. The M2.

This chart and the home-value chart cover the same stretch of time. Here's what jumped out at me when I laid them side by side — and side by side is how I do everything, ask any of my sellers.

Back during the 2003-to-2008 run, the money supply barely budged. Home values climbed anyway — that was credit loosening up, people getting loans they had no business getting — and we all know how that movie ended. It wasn't built on anything real.

Now look at the COVID run-up. That one came from demand — low, low, low interest rates pulling everybody off the sidelines all at once. And this time the money supply grew right alongside it. Almost line for line. Both peaked in April of 2022. Both came down after. And both are climbing again. Makes me wonder if that's the difference — whether this run has held for over six years, where the last one couldn't make it five, because there's actual money underneath it this time.

Okay, so when do they come down?

What goes up must come down. I believe that, I really do. The question was never if — it's always been when. And anybody who tells you they can time the market to the day with a straight face? I'd smile politely and keep one hand on my purse.

I'm not going to pretend I've got the date circled on a calendar, because I don't. What I've got is a hunch worth talking about — that this money-supply piece is quietly holding values up in a way the last bubble never had going for it. So I'm genuinely curious what you think. Does that hold water?

Because here's where I land: what's it going to take to bring the money supply back down? Whatever that turns out to be, I'd bet home values come down right next to it — not a minute before.

And that's exactly the kind of thing I'd rather talk through with you, in person, looking at your situation and your neighborhood — not in the abstract. That's the whole job. I'll take the homework and the worry off your plate. You just tell me where you're headed.

Hold the phone — foreclosures are climbing?

They are. And that one deserves its own conversation. I'll walk you through it next.